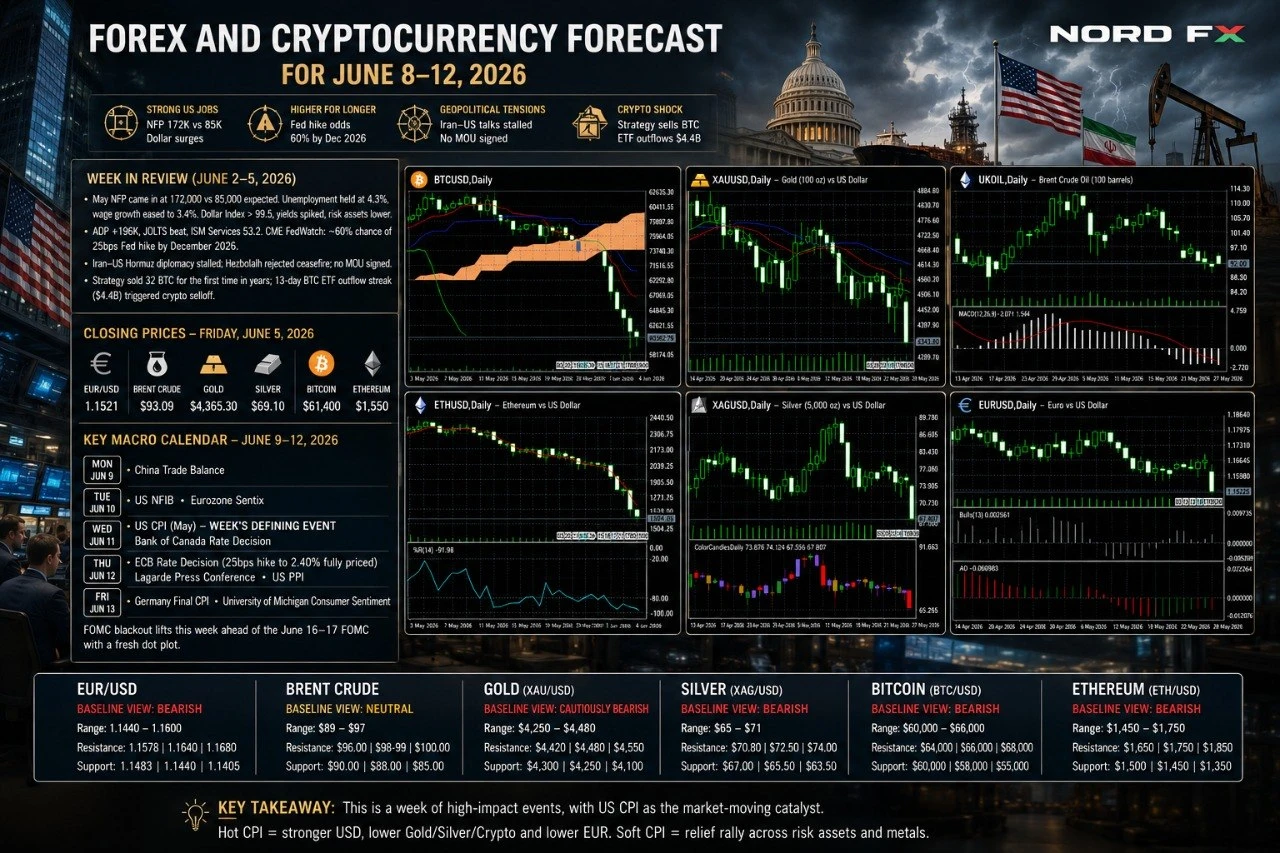

6月2日至5日当周,宏观经济遭受决定性冲击。周五公布的5月非农就业数据达到172,000——几乎是市场预期85,000的两倍——4月数据则上修至179,000。失业率维持在4.3%,年薪资增速回落至3.4%。亮眼数据推动美元指数飙升至99.5上方,美债收益率大幅攀升,风险资产全面下跌。本周早些时候,ADP就业数据以+196,000超出预期,JOLTS职位空缺数意外走高,ISM服务业PMI录得53.2且已付价格分项走强。CME美联储观察工具目前将2026年12月前美联储加息25个基点的概率定价为约60%——为3月以来最高。

地缘政治方面,伊朗与美国就霍尔木兹海峡的外交斡旋陷入僵局:德黑兰拒绝确认谈判取得进展,真主党否决了美国斡旋的以色列-黎巴嫩停火协议,谅解备忘录未能签署。加密货币市场方面,Strategy(前身为MicroStrategy)数年来首次出售32枚比特币——规模微不足道,但象征意义极为深远——引发多头仓位连环平仓。叠加现货比特币ETF创纪录连续13天净流出(共44亿美元),整个加密货币市场崩跌至数月低位。

2026年6月5日(周五)收盘价:

欧元/美元 – 1.1521 | 布伦特原油 – 93.09美元 | 黄金(XAU/USD)– 4,365.30美元 | 白银(XAG/USD)– 69.10美元 | 比特币 – 61,400美元 | 以太坊 – 1,550美元

6月8日至12日重要宏观日历:周一:中国贸易差额。周二:美国NFIB;欧元区Sentix。周三:美国5月CPI——本周最关键事件;加拿大央行利率决议。周四:欧洲央行利率决议(加息25个基点至2.40%已被充分定价);拉加德新闻发布会;美国PPI。周五:德国最终CPI;密歇根大学消费者信心指数。美联储"静默期"解除,为6月16日至17日FOMC会议及最新点阵图做准备。

欧元/美元

欧元/美元收于1.1521(5月29日前收盘价:1.1660;52周区间1.1343–1.2079;日内评级:强力卖出)。非农数据冲击下,该货币对决定性跌破200日均线及1.1580–1.1600支撑区间,单周下跌约1.4%。RSI已跌至35–38——日线图呈超卖状态,但周线图仍有进一步下行空间。欧洲央行会议纪要已显示政策制定者讨论过4月加息,市场已充分定价欧洲央行将于6月12日加息25个基点。然而,加息已被定价,现在决定性的未知变量是周三的美国CPI数据。

关键催化剂: 美国CPI(周三):市场预期约4.2%(同比),此前4月意外录得3.8%。若高于4.5%则明显利好美元,目标指向1.1440;若低于4.0%则打开反弹空间,目标1.1580–1.1620。欧洲央行(周四):鹰派指引暗示进一步加息将利好欧元;"加息一次即止"信号则延续跌势。美国PPI(周四)和密歇根大学情绪指数(周五)为次要因素。

阻力位:1.1578/1.1600、1.1640、1.1680 │ 支撑位:1.1483/1.1497、1.1440、1.1405/1.1417

基准观点:偏空。非农驱动的跌破1.1580维持4月以来的下行趋势。任何CPI超预期均带来不对称的下行风险。CPI低于预期是最明确的欧元多头情景。基准区间:1.1440–1.1600。

布伦特原油

布伦特原油收于93.09美元(周涨幅+2.2%;52周区间58.72–126.41美元;日内信号:卖出)。尽管市场情绪避险,布伦特仍上涨,原因在于伊美外交谈判完全陷入僵局:德黑兰否认近期有进展,真主党拒绝停火,谅解备忘录未能签署。EIA数据确认美国原油库存连续六周下降。负面方面,中国原油进口量降至10年低位,发出重大需求侧逆风信号,而非农数据驱动的全球增长预期重新定价也带来压力。100日均线(约98–99美元)仍为上方阻力。

关键催化剂:伊朗/霍尔木兹——最主要的二元变量:停火信号将推动布伦特跳空至88–85美元;霍尔木兹局势升级则将目标重定至97–100美元。中国贸易数据(周一)。EIA库存(周三)。美国CPI(周三):数据偏热暗示全球需求收紧;低于预期则温和利好油价。

阻力位:96.00美元、98.00–99.00美元(100日均线)、100.00美元 │ 支撑位:90.00美元、88.00美元、85.00美元

基准观点:中性,受地缘政治主导。连续六周库存下降和IEA持续的供应短缺评估在88–90美元附近形成支撑底部。中国需求疲软和增长预期重新定价抑制上行空间。周末外交突破是唯一可能将布伦特推至88美元以下的事件。基准区间:89–97美元,取决于谅解备忘录/霍尔木兹局势解决。

黄金(XAU/USD)

黄金现货收于4,365.30美元——2026年以来最低收盘价——较4,593.00美元单周下跌约4.9%(52周区间3,247.86–5,595.46美元;日内评级:强力卖出)。黄金较1月接近5,595美元的历史高位低约22%,但较去年同期仍上涨+31%。此次抛售反映了非农驱动的美元飙升、美国10年期国债收益率接近4.60%以及霍尔木兹灾难性尾部风险的部分消退。高盛(目标价5,400美元)和摩根大通(目标价5,900美元)的年底目标维持不变,由央行创纪录购金和去美元化资金流动支撑。黄金目前处于关键关口:守住4,300–4,370美元区间或跌破指向4,100美元。

关键催化剂: 美国CPI(周三):高于4.5%将巩固美联储加息预期,目标指向4,200–4,250美元;低于4.0%触发有意义的反弹至4,480–4,520美元,重开降息讨论。欧洲央行加息(周四)——鹰派指引和欧元反弹带来美元小幅走弱,助黄金企稳。美国PPI和密歇根大学通胀预期(周四/五)为辅助因素。

阻力位:4,420美元、4,480–4,500美元、4,550美元 │ 支撑位:4,300美元、4,250美元、4,100美元

基准观点:短期谨慎偏空。动能持续偏负,但日线图深度超卖状态和长期结构性多头逻辑(央行购金、去美元化)限制了下行空间。CPI低于预期是主要的复苏催化剂。基准区间:4,250–4,480美元。长期多头目标(5,400–5,900美元)依然有效。

白银(XAG/USD)

白银现货收于69.10美元——2026年3月底以来最低——较76.17美元单周下跌约9.3%(52周区间31.64–121.67美元;日内评级:强力卖出)。白银是跌幅最大的贵金属,跌幅超过黄金,原因在于其两大驱动力同时失效:贵金属属性方面,美元走强和美联储鹰派立场造成冲击;工业金属属性方面,中国进口数据疲软造成冲击。金银比已扩大至接近63。RSI深度超卖但动能仍强劲偏负,20日布林均线(约77.50美元)现已远在上方成为阻力。

关键催化剂: 中国贸易数据(周一)——近期最强大的正面催化剂:进口强劲暗示工业需求复苏。美国CPI(周三):数据偏热使白银承压;低于预期则指向73–75美元目标。欧洲央行加息(周四)——通过欧元回升带来边际利好。密歇根大学5年通胀预期(周五)。

阻力位:72.00美元、74.00美元(20日EMA)、76.00美元 │ 支撑位:67.00美元、65.00美元、60.00美元

基准观点:偏空至中性。跌破73美元后再跌破70美元将开启65–67美元区间。CPI低于预期是最明确的反弹催化剂,但此前每个支撑位现已成为阻力位。基准区间:65–73美元。任何风险偏好改善的催化剂均可能使金银比急剧收窄。

比特币(BTC/USD)

比特币收于约61,400美元(盘中低点59,099美元——2024年10月以来最低;单周下跌16%,此前为73,565美元;52周区间60,187–126,186美元)。BTC较其2025年10月126,198美元的历史高位低逾51%。此次抛售是多因素共同作用的结果:Strategy出售32枚BTC——规模可忽略不计,但象征意义极为沉重——引发连环清算。连续13天ETF净流出(44亿美元)是ETF上市以来历时最长的一次。周五非农数据驱动的美债收益率飙升放大了压力。200日EMA(约82,000美元)连续六周压制反弹。正面方面,ETF于周四净流入300万美元打破了连续流出记录,交易所比特币储备维持在近7年低位,CLARITY法案(参议院银行委员会以15:9通过)仍是重要的结构性利好。

关键催化剂:周末伊朗/霍尔木兹消息——风险偏好改善可能触发急剧的空头回补反弹。美国CPI(周三):数据偏软将重新打开降息叙事——这是比特币最强的宏观正面因素,目标指向65,000–68,000美元;数据偏热则目标下移至57,000–55,000美元。美联储"静默期"解除——美联储官员发言可能撼动市场。CLARITY法案——国会任何进一步进展均带来不对称的正面影响。

阻力位:63,000美元、65,000美元、68,000美元 │ 支撑位:59,000–60,000美元(关键底部/52周低位区间)、55,000美元、52,000美元

基准观点:在65,000美元以下谨慎偏空。CPI低于预期是触发有意义反弹的最明确催化剂。持续收盘于59,000美元以下将开启55,000美元。基准区间:58,000–65,000美元。

以太坊(ETH/USD)

以太坊收于约1,550美元(单周下跌22.2%,此前为1,992美元;52周区间1,388.12–4,955.90美元;日内评级:强力卖出)。以太坊表现大幅弱于比特币——这在风险规避期间是一种通常会持续的规律,因资金向市值更大的资产集中。ETH上周跌破2,000美元后,周五又相继失守1,800美元、1,700美元和1,650美元。以太坊目前仅比52周低位1,388美元高约12%。现货ETH ETF连续逾10天净流出,5月以来流出规模达5.7亿美元。50日EMA(约2,175美元)和200日均线(约2,200美元)仍是遥远的上方阻力。渣打银行预计以太坊2026年底将达4,000美元。CLARITY法案——直接涉及ETH商品与证券属性界定——仍是最具不对称性的正面催化剂。

关键催化剂: 美国CPI(周三):低于4.0%则目标指向1,700–1,800美元;高于4.5%则52周低位1,388美元将面临考验。欧洲央行加息(周四)——通过风险偏好改善带来温和利好。CLARITY法案——参众两院任何投票均是最具不对称性的以太坊专属催化剂。

阻力位:1,650美元、1,750美元、1,850美元 │ 支撑位:1,500美元、1,450美元、1,388美元(52周低位)

基准观点:偏空。多个关键支撑位相继迅速失守,结构严重受损,ETH/BTC比率持续恶化。反弹至1,850美元上方需要CPI低于预期且欧洲央行政策偏向建设性。CLARITY法案是最强大的独立上行催化剂。基准区间:1,450–1,700美元。

总结

6月8日至12日当周是2026年迄今为止宏观意义最为重大的一周,集中了美国CPI(周三)、欧洲央行利率决议(周四,加息25个基点至2.40%已被充分定价)和美国PPI(周四)——这一切距6月16日至17日美联储会议及最新点阵图仅数日之遥。美联储"静默期"本周解除,美联储官员可能重新发声并放大CPI和欧洲央行的市场反应。伊朗/霍尔木兹二元变量仍是未列入日历的通配符:周末外交突破将使布伦特跳空至85–88美元,缓解美元压力,并在所有资产类别引发风险偏好反弹。

周三的美国CPI是本周的决定性催化剂。若数据高于4.5%(偏热):欧元/美元面临1.1440风险,黄金重测4,200–4,250美元,比特币跌破59,000美元,白银目标65美元,以太坊接近52周低位。若数据低于4.0%(偏软):欧元/美元反弹至1.1580–1.1620,黄金收复4,480–4,520美元,比特币目标65,000–68,000美元,白银尝试收复73–75美元。周四欧洲央行加息已被定价——关键在于拉加德的指引。鹰派信号:利好欧元。鸽派"一次加息即止":无论如何欧元/美元将继续下行。

欧元/美元报1.1521:偏空,CPI偏热时目标1.1440,偏软时目标1.1580–1.1600。布伦特报93.09美元:89–97美元,受地缘政治驱动。黄金报4,365.30美元:徘徊于关键支撑4,300–4,370美元。白银报69.10美元:深度超卖,基准区间65–73美元。比特币报61,400美元:守住59,000–60,000美元底部。以太坊报1,550美元:CLARITY法案和CPI低于预期是主要的多头触发因素。

NordFX分析团队

免责声明:本材料不构成投资建议或金融市场操作指南,仅供参考。金融市场交易存在风险,可能导致所有存入资金的完全损失。

返回 返回