People often imagine forex trading taking place on a single exchange floor, with one official price and one central order book. That is not how the foreign exchange market works. Most forex trading is done “over the counter” (OTC), which means transactions happen through a network of banks, liquidity providers, brokers, and electronic venues rather than through one central exchange.

Understanding where forex trading is done is more than trivia. It helps you make sense of why prices can differ slightly between providers, why spreads widen at certain times, why liquidity changes through the day, and why execution quality depends on market structure. Once you see the market as a global network, many practical trading questions start to answer themselves.

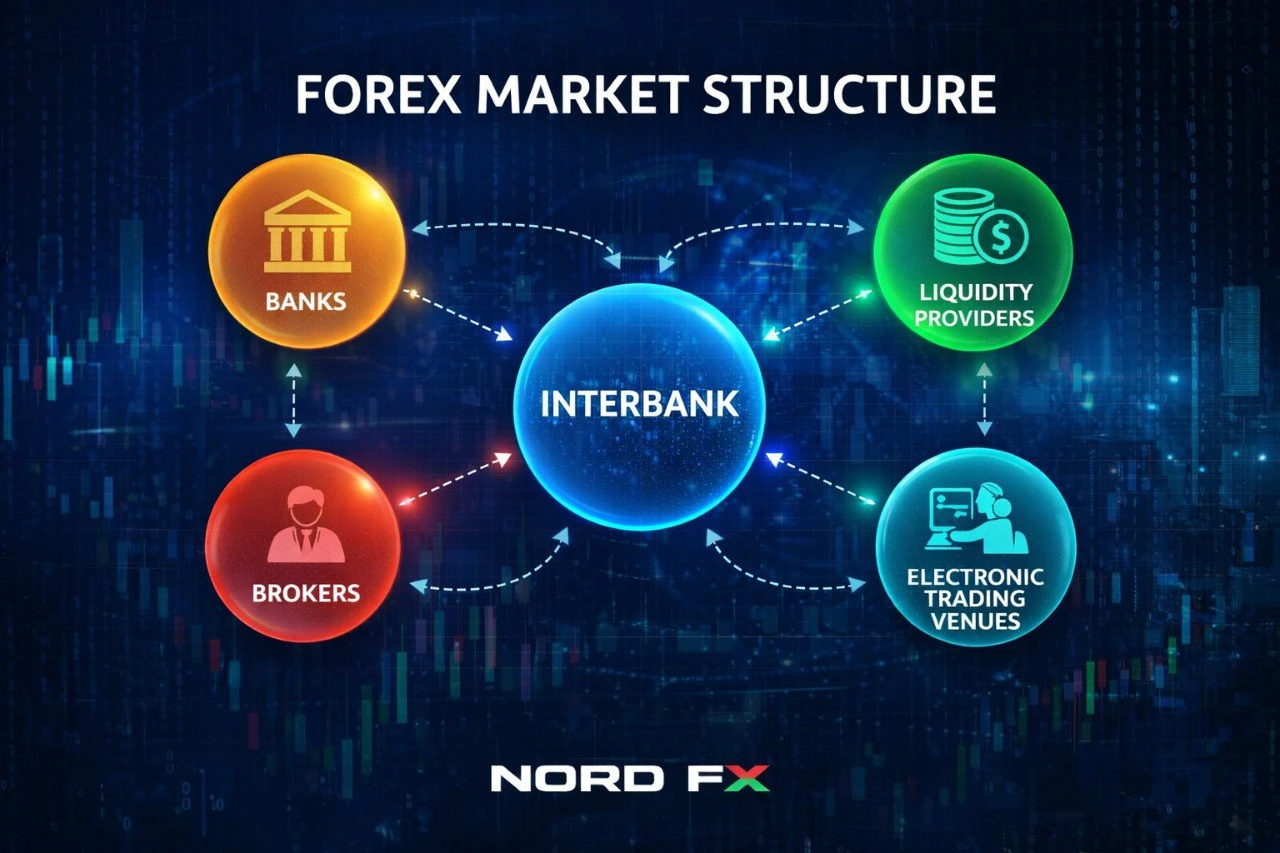

The forex market is a network, not a place

Forex is the world’s largest financial market because currencies are constantly exchanged for trade, investment, travel, hedging, and speculation. Unlike shares listed on a stock exchange, currencies do not “live” on a single venue. Instead, prices are formed through continuous quoting and dealing across multiple participants.

At the centre sits the interbank market - large banks and institutions that quote prices to each other and trade in very large size. Around that core are non-bank liquidity providers, electronic trading venues, and prime brokers that help route flows and manage settlement. Retail traders do not typically access the interbank market directly; they trade through a broker, using platforms that connect them to streamed pricing and execution.

So, when someone asks, “Where is forex trading done?”, the most accurate answer is: it is done across a decentralised global network of dealing relationships and electronic systems, operating 24 hours a day from Monday to Friday.

The interbank market: where the largest flows meet

The interbank market is where major banks trade currencies with each other, quoting two-way prices (bid and ask) and managing risk from client flows. Trades can be arranged directly between banks or facilitated by intermediaries.

Two key ideas matter here.

First, pricing is competitive and continuous. Multiple institutions quote simultaneously, and the best available prices can change in fractions of a second as orders, news, and risk limits shift.

Second, liquidity is not uniform. The deepest liquidity usually appears in major pairs such as EUR/USD, USD/JPY, and GBP/USD during the busiest overlapping trading hours. Liquidity tends to thin out around market rollovers, holidays, and during quieter session handovers, which can affect spreads and slippage.

If you want a clearer sense of why liquidity conditions matter to execution and trading costs, NordFX has a helpful explainer on liquidity mechanics here: Understanding Market Liquidity Across Assets.

Electronic venues and ECNs: “marketplaces” inside the network

Over the past two decades, a significant share of institutional forex trading has moved onto electronic venues. These include multi-bank platforms and ECN-style systems that aggregate quotes from several liquidity sources. They are not “exchanges” in the classic stock-market sense, because forex spot remains OTC, but they function as organised marketplaces where participants can interact electronically.

These venues matter because they help explain two practical realities:

Price is not always identical everywhere. Different pools of liquidity can show slightly different best bids and offers at the same moment, especially in fast markets.

Execution depends on routing. Where your order goes - and how it is matched - can influence the final fill, particularly during volatility spikes.

Retail traders normally experience this through the broker’s pricing and execution model. It is one reason it can be useful to understand why prices and spreads vary between providers. NordFX covers the main drivers in a clear “How Trading Works” article: Why do prices and spreads differ between brokers?.

Retail forex: where most individual traders actually trade

Most individuals trade forex via a broker offering CFDs or margin-based forex products. In that setup, the “place” where you trade is effectively a combination of:

the broker’s pricing streams, sourced from liquidity providers and/or internal risk systems, and

the trading platform, which is the interface that displays quotes and sends your orders.

For a retail trader, the important question is less “Which building does forex trade in?” and more “What market access does my broker provide, and how is my trade executed?”

A broker may use external liquidity providers, internal matching, or a hybrid approach. Each model has implications for spreads, commissions, execution speed, and behaviour during high-volatility events. None of this changes the core fact that the underlying market is decentralised; it simply describes how your trades are connected to that market.

If you want to see how trading access is typically packaged for different trader profiles, you can review the account structures and platform options here: All Accounts | NordFX Trading Accounts.

Trading platforms: the “where” you interact with the market

From a user perspective, forex trading is “done” inside the platform you use, even though the real market sits behind it. The platform handles charting, order tickets, risk controls, and trade management, while connecting to the broker’s execution environment.

MetaTrader remains the most familiar choice in retail forex. If you trade through NordFX, you can explore the platform environment and how it supports forex and other markets on the platforms page: Trading Platforms | MT4 and MT5.

Thinking about the platform as part of the “where” is useful because many practical outcomes are platform-shaped. Order types, how stop-loss and take-profit levels are set, how partial fills are handled, and how you monitor margin all live in the platform layer. The market may be global and decentralised, but your trading experience is local to the tools you use.

Time zones and trading sessions: where liquidity concentrates

Forex trades around the clock during the working week because the market follows the sun. Activity rotates through the major financial centres, and liquidity builds when large regions overlap.

The market is commonly described in four broad sessions: Sydney, Tokyo, London, and New York. Those names are shorthand, not strict borders, but they help explain typical liquidity patterns.

Liquidity often increases when London opens because it is a dominant centre for global FX dealing. The period when London and New York overlap is frequently the most active window for many major pairs, with tighter spreads and faster order matching under normal conditions. Activity can feel slower during late US hours and early Asia, especially for pairs that are not closely linked to Asian flows.

This matters because the same strategy can behave differently depending on when you trade it. Breakouts, for example, may be more reliable when liquidity is strong, while range behaviour can appear more often in quieter periods. Spreads can also widen outside peak hours, which changes the effective cost of entry and the distance your trade must move to become profitable.

Is forex trading done on exchanges at all?

Spot forex - the market most retail traders associate with “forex” - is primarily OTC. However, some currency products are exchange-traded, and it helps to separate the categories.

Currency futures, for instance, are standardised contracts traded on regulated exchanges. They have central clearing and an order book, which makes them structurally different from OTC spot. Options on currencies can also trade on exchanges, though a large institutional options market exists OTC as well. These exchange-traded markets can influence pricing and hedging behaviour, but they do not replace the OTC nature of the global spot market.

So, if your question is “Is there any exchange where forex is done?”, the honest answer is: yes, for certain currency derivatives, but the core global market for spot FX remains decentralised.

What this means for trading decisions

Understanding where forex trading is done helps you evaluate trading conditions more realistically.

It becomes easier to interpret spreads because you recognise they reflect liquidity, risk, and execution structure rather than a single universal fee. It becomes easier to plan trading times because you understand why liquidity clusters around session overlaps. It becomes easier to think about risk during major news releases because you recognise that quotes can change rapidly across multiple venues at once, and order filling depends on available liquidity at that moment.

Most importantly, it encourages you to treat forex as a real market with real microstructure, not a simple price feed. The more your expectations match how the market actually works, the more confidently you can choose instruments, timings, order types, and risk limits.

Final thoughts

Forex trading is done everywhere and nowhere in the traditional sense. There is no single exchange floor where “the” forex price is set. The market exists as a global OTC network, anchored by the interbank system, expanded by electronic trading venues, and accessed by individuals through brokers and platforms.

If you keep that picture in mind, you will find it easier to understand execution, pricing differences, and the daily rhythm of volatility and liquidity - and you will be better equipped to trade thoughtfully rather than mechanically.

Risk reminder: forex and CFDs involve leverage and can result in losses as well as gains, so risk management and position sizing matter just as much as market direction.